Source: U.S. Navy

Source: U.S. Navy

The Navy’s newly released long-range shipbuilding plan carries an ambitious price tag: around $1.2 trillion for new ship construction over 30 years, more than 30 percent above what the previous plan projected. Behind that ambitious plan is a new class of battleships that the service envisions as the nuclear-powered, missile-laden centerpiece of its future force, branded the “Golden Fleet.” The new plan introduces notable changes to shipbuilding strategy, industrial base investment, and sustainment policy. But the scale of the investment, paired with some optimistic assumptions, raises real questions about whether the Navy can deliver on what it’s promising.

The Battleship That Could Sink the Budget

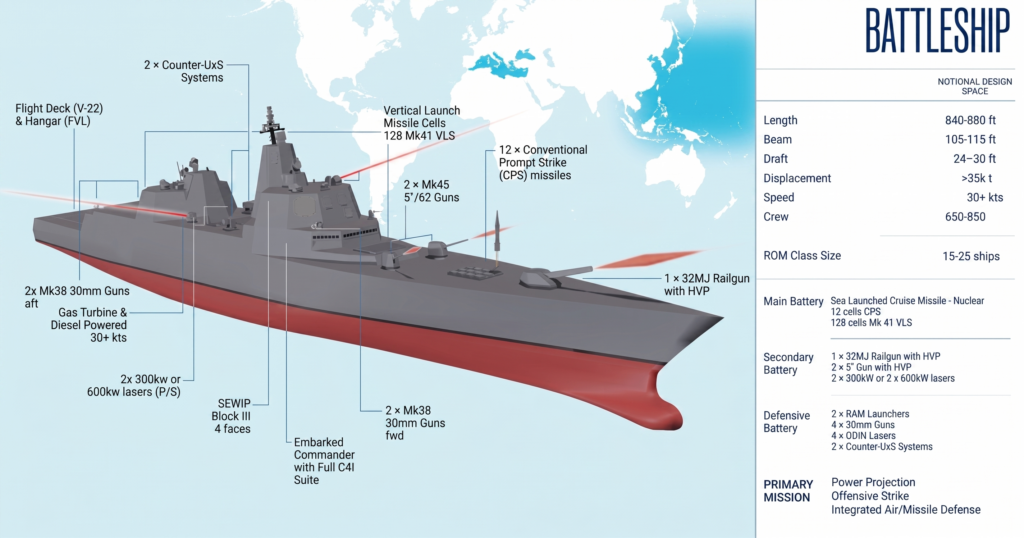

The most significant change to the Navy’s long-term shipbuilding plans is the introduction of a new class of battleships, large platforms intended to host a high volume of missile cells, directed energy weapons, traditional naval artillery, railguns, and command and control capabilities. The service plans for the ship to be nuclear powered, and it may even carry theater nuclear weapons to create “difficult strategic calculations for adversaries.” The first battleship would be procured in FY28, but it won’t be delivered until FY36, assuming an on-time delivery schedule. The battleship is being pursued in place of a follow-on DDG(X) destroyer, but the Navy will continue buying DDG 51 destroyers concurrently with the new battleship.

Perhaps the biggest concern with the battleship is costs. The Navy estimates the lead ship will cost over $17 billion, with an average cost of $14.5 billion for the first three ships. The service plans to spend $43.5 billion over the Future Years Defense Program on the first three ships in the class. For comparison, it will cost around $25.3 billion to procure seven DDG 51 destroyers over the same period. Investment in the battleship substantially raises the overall cost of the Navy’s shipbuilding portfolio without expanding battle force inventory in the near-term.

As recently as April, Navy officials suggested it would be unlikely that the new battleship would be nuclear powered. The shift to nuclear power introduces cost and complexity, as well as industrial base limitations. Huntington Ingalls Industries’ Newport News Shipbuilding is the only U.S. shipbuilder constructing nuclear-powered surface warships (Ford class aircraft carriers), while Newport News and General Dynamics’ Electric Boat are responsible for building nuclear-powered submarines. Both shipyards are already facing significant workloads even without the addition of a new battleship class.

Source: CRS via U.S. Navy

Source: CRS via U.S. Navy

The battleship also raises design and operational questions. For one, the ship is intended to carry a variety of weapons that aren’t fully developed or combat-proven, such as railguns, ship-based hypersonic missiles, and directed energy platforms. The Ford class struggled with cost growth and development issues because of the wide range of new technologies introduced in the class. It’s likely the battleship will face some of the same challenges. It’s also unclear how well the new class will fit into the Navy’s Distributed Maritime Operations approach, a concept that envisions maritime assets dispersed over a large area to make them harder to detect and defeat. Concentrating so much firepower on a single ship makes it a prime target in a conflict with a country like China, and losing a single battleship in combat would be a significant blow to the U.S. fleet.

The name of the battleship alone raises questions. Called the Trump class (BBGN), the planned ship deviates from the Navy’s traditional ship naming conventions. Historically, aircraft carriers are named for former presidents, while battleships were named after states. The optics of naming a new class of ships after a sitting president paints it as a pet project of the current administration, which could impact congressional support. Further, the long timeframe needed to design and build the ships means future administrations will have to sign onto the plan. In the end, it’s questionable if the Trump class will be built at scale, if at all.

More Money, Fewer Ships

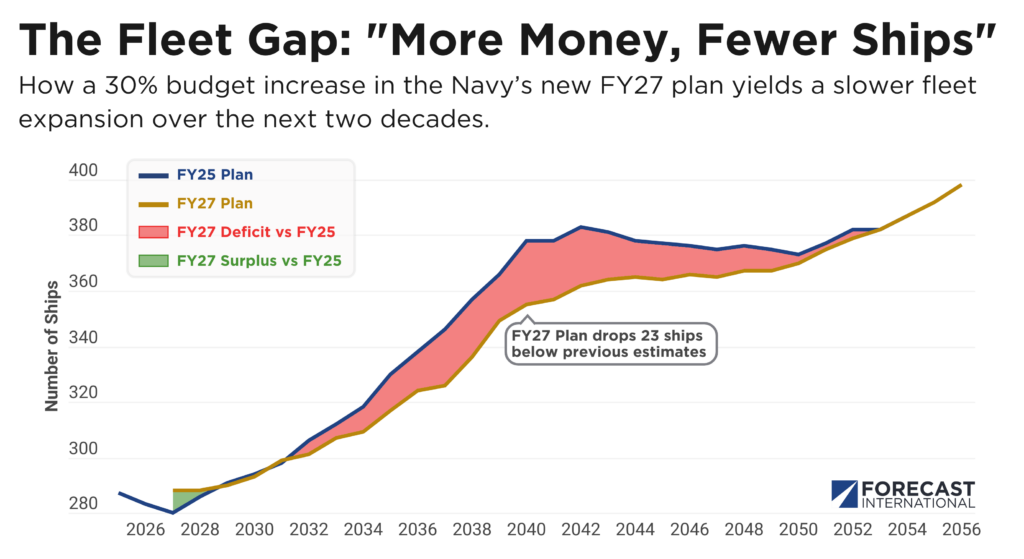

The new battleship introduces concerning dynamics for the Navy’s budget and the size of its future fleet. The FY25 shipbuilding plan, released during the Biden administration, outlined annual new ship construction costs of around $30 billion, or approximately $900 billion over 30 years. These figures only reflect new construction costs, and don’t account for the entire annual shipbuilding and conversion budget. The new FY27 plan anticipates average new ship construction costs of around $39.6 billion per year, or $1.2 trillion over 30 years. The new price tag is more than 30 percent higher than the previous plan, due in large part to the expensive battleship.

However, the higher cost of the shipbuilding plan doesn’t result in more ships compared to the previous plan. While both the FY25 and FY27 plans approach a fleet of 400 battle force ships in the mid-2050s – up from 291 today – the FY27 strategy results in a lower battle force inventory through nearly the entire 30-year period, when compared to previous projections. When lined up against figures from the previous administration, the new plan maintains a lower number of small surface combatants and auxiliaries into the 2050s, while the large surface combatant inventory falls short starting in the mid-2030s and into the early 2040s. Only after the new battleship comes online does the large surface combatant force begin to exceed the planned inventory under the FY25 strategy.

Conversely, the new plan yields an expanded inventory of amphibious warfare vessels. Minor changes to delivery and retirement timelines provide the Marines with between one and three more large amphibious warships (LSD/LPD and LHD/LHA) in any given year compared to the FY25 plan.

A Shipbuilding Industry Already Stretched Thin

The shipbuilding industrial base has been pushed to its limits, and lingering supply chain and workforce issues are still contributing to rising costs and schedule delays. The strategy doesn’t try to gloss over these issues and outlines several initiatives aimed at facilitating ship construction.

Perhaps the biggest factor will be increased adoption of distributed shipbuilding methods. Rather than building a ship in a single yard from the ground up, distributed manufacturing relies on different yards building modules or components of various ships, at which point all of the pieces are assembled at a single shipyard. The Navy says that around 10 percent of work is currently performed at distributed sites, with a goal of increasing that figure to 50 percent. This approach will increase reliance on modular construction, but it will still require continued investment in a robust supply chain and shipyard infrastructure.

To that end, the Navy is calling for industry to invest in its own infrastructure and workforce to help facilitate construction goals. For its part, the service said it needs to provide consistent demand signals to justify those investment efforts.

The strategy also supports some overseas construction, such as for some ship modules and hull structures, as well as for some auxiliaries. Congress has always been protective of domestic shipbuilders, and some resistance has already surfaced against any effort to offshore any amount of ship construction. This sourcing shift will likely emerge as a contentious issue during FY27 National Defense Authorization Act (NDAA) deliberations. Regardless of the status of moving any construction overseas, the U.S. has already seen increased foreign investment, which will help bolster domestic capacity.

Sustainment: The Hidden Cost Problem

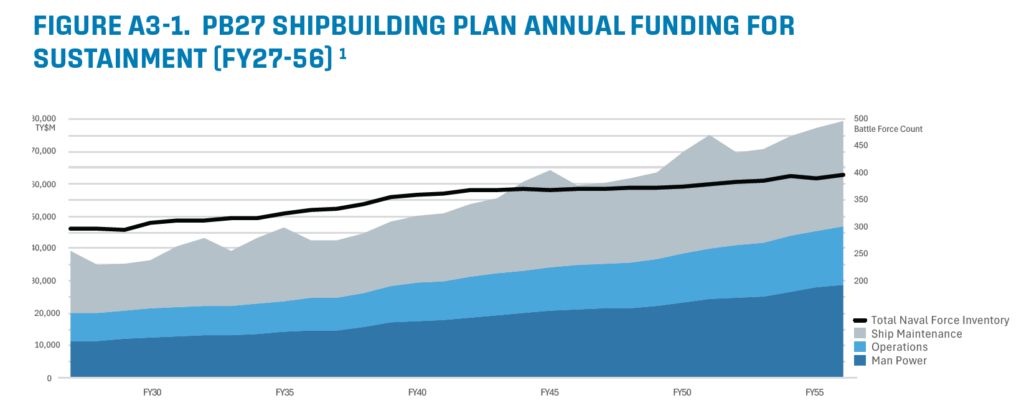

The Navy expects its fleet sustainment costs (personnel, operations, and maintenance) to grow by around 2.5 percent annually over the next 30 years, which aligns closely with inflation and growth projections in the FY25 plan. However, these projections may be overly optimistic.

Looking back at the FY20 shipbuilding plan, developed when the Navy was attempting to grow its fleet by around 18 percent (from 300 to 355 ships), projected annual sustainment growth spiked to approximately 3.6 percent during the active growth phase, flattening to 2.3 percent only after the fleet stabilized at 355 ships. In contrast, the current FY27 strategy anticipates a massive 40 percent expansion in fleet size, yet assumes a 2.5 percent sustainment growth rate throughout the next 30 years. It should be noted that the Navy’s long-term sustainment estimates merely reflect FY31 funding levels inflated forward using Pentagon inflation indices. Nevertheless, sustainment costs could easily grow more rapidly than what the chart assume as the fleet expands, which could put pressure on other areas of the budget, including ship construction. These sustainment estimates also don’t account for other long-range costs like modernization and ordnance, infrastructure and training, and aviation detachments.

The new shipbuilding plan does outline several efforts to lower maintenance costs, such as increasing the use of AI tools for predictive maintenance, using smaller and more frequent maintenance availabilities, adopting new maintenance contracting practices to provide yards with increased planning time, and relying on sailors to conduct more advanced maintenance work. It’s unclear if these efforts will result in the desired maintenance savings, but even if they do, personnel and operations costs will still grow faster as the fleet increases in size.

Promises vs. Results

The new shipbuilding plan is candid about the Navy’s past failures, including a stagnant fleet, schedule slips, and overly optimistic cost estimates that government watchdogs have flagged repeatedly for years. That self-awareness is welcome, but acknowledging past mistakes and actually breaking those habits are different things.

The Navy’s new shipbuilding plan highlights the importance of both speed and scale, but it struggles to find a balance between those concepts and their impact on the future fleet. The Navy is trying to move rapidly on its new FF(X) frigate fleet after struggling with small surface combatants since the inception of the Littoral Combat Ship program nearly 25 years ago and the recent termination of the Constellation class, which the FF(X) is slated to succeed. However, initial versions of the ship won’t feature internal vertical launch systems, instead relying on containerized weapons. Budget documents have already outlined plans to integrate a VLS into future versions of the ship, which raises questions about requirements, capabilities, and design changes that have plagued small surface combatant programs over the years. On the lower end of the capability spectrum, new strategy outlines a long-term Medium Unmanned Surface Vessels (MUSVs) acquisition plan that includes buying 36 vessels in FY26, but the service has struggled to determine the best approach to develop and integrate maritime drones into the fleet. Meanwhile, the battleship reflects a tremendous investment in an asset that comes with its own operational concerns, all while putting immense pressure on the budget.

The industrial base investments represent the most promising aspect of the shipbuilding plan. The Navy rightly cites the limitations of the current domestic shipbuilding infrastructure. Increasing modularity and distributed shipbuilding can go a long way to meeting projected demand, but sustained capital allocation is required to increase capacity and strengthen supply chains over the long-term. Part of the solution is additional investment from shipbuilders themselves, and the Navy plans on providing consistent demand signals to make that investment worthwhile for shipbuilders. However, the complex tug of war between Navy planners, the White House, and Congress can result in major programmatic shifts in any given year. Those changes can have long-lasting ripple effects, meaning stability and consistency are paramount. If the Navy cannot translate its ambitious projections into affordable and executable programs, the “Golden Fleet” could ultimately become remembered more for its promises than its results.

Shaun's deep-rooted interest in military equipment continues in his role as a senior defense analyst with a focus on the United States. He played an integral role in the development of Forecast International's U.S. Defense Budget Forecast, an interactive online product that tracks Pentagon acquisition programs throughout the congressional budget process. As editor of International Military Markets – North America, Shaun has cultivated a deep understanding of the vast defense markets in the United States and Canada. He is a regular contributor to Forecast International's Defense & Security Monitor blog and has co-authored white papers on global defense spending and various military programs.

image sources

- USS_Defiant_BBGN: U.S. Navy

- BBGN_Design: CRS via U.S. Navy